Atal Pension Yojana 2026: How This Government Scheme Is Securing Retirement for Millions of Indians

The Government of India’s Atal Pension Yojana (APY) continues to emerge as one of the country’s most important social security schemes for workers in the unorganized sector. Designed to provide guaranteed monthly pension benefits after retirement, the scheme has gained massive popularity among low-income earners, small business owners, labourers, farmers, and self-employed individuals across India.

As inflation and financial uncertainty increase, more Indians are turning toward long-term pension plans to secure their future. In recent months, Atal Pension Yojana has witnessed strong growth in new registrations, with millions of subscribers joining the scheme for guaranteed retirement income and government-backed security. (npscra.nsdl.co.in)

The scheme is managed by the Pension Fund Regulatory and Development Authority under the supervision of the Government of India and has become a major pillar of India’s financial inclusion strategy.

What Is Atal Pension Yojana?

Atal Pension Yojana is a government-backed pension scheme launched in 2015 to help citizens from the unorganized sector build a financially secure retirement.

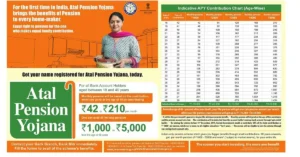

The scheme guarantees a fixed monthly pension after the age of 60 depending on the subscriber’s contribution and chosen pension amount. Subscribers can receive monthly pensions ranging from ₹1,000 to ₹5,000.

The main objective of APY is to encourage long-term savings among people who may not have access to formal retirement plans or employer-sponsored pensions.

Why Atal Pension Yojana Is Becoming More Popular

Financial experts believe the rising popularity of APY is linked to growing awareness about retirement planning and economic security.

Several factors are driving enrollment growth:

- Guaranteed monthly pension

- Low monthly contribution

- Government-backed scheme

- Easy bank account integration

- Auto-debit contribution system

- Tax benefits under income tax rules

- Security for families after subscriber’s death

For many Indians working in small businesses, agriculture, construction, transportation, or informal jobs, APY provides a simple and affordable retirement solution.

The scheme has especially become popular in rural India where formal pension coverage remains limited.

Who Can Apply for Atal Pension Yojana?

The eligibility criteria for APY are straightforward, making it accessible to millions of Indians.

A person can join APY if they:

- Are an Indian citizen

- Have a savings bank account or post office account

- Are between 18 and 40 years of age

- Possess a valid Aadhaar number and mobile number

Once enrolled, the subscriber must regularly contribute until the age of 60 to receive pension benefits.

According to official guidelines, individuals who are income taxpayers are not eligible for government co-contribution benefits under APY. (india.gov.in)

How the Pension Amount Works

One of the key attractions of APY is the guaranteed pension structure.

Subscribers can choose a monthly pension amount from:

- ₹1,000

- ₹2,000

- ₹3,000

- ₹4,000

- ₹5,000

The monthly contribution depends on:

- Entry age

- Desired pension amount

- Contribution period

For example, younger subscribers contribute lower monthly amounts because they invest for a longer period.

A person joining at age 18 for a ₹5,000 monthly pension may need to contribute around ₹210 monthly, while someone joining at age 35 would need significantly higher contributions. (npscra.nsdl.co.in)

Government Support Makes APY Attractive

One major reason for APY’s success is government backing.

Unlike market-linked investment schemes where returns fluctuate, Atal Pension Yojana provides a guaranteed pension amount after retirement. This creates confidence among low-income earners who prefer stable financial planning over risky investments.

The government had initially offered co-contribution benefits for eligible subscribers who joined within specified timelines. Although that limited-time benefit ended, APY still remains highly attractive because of its simplicity and security.

Financial advisors say APY works best for people seeking disciplined long-term savings without exposure to stock market volatility.

Tax Benefits Under Atal Pension Yojana

Subscribers also receive income tax benefits under Section 80CCD of the Income Tax Act.

Benefits include:

- Tax deductions on contributions

- Additional deduction under Section 80CCD(1B)

- Retirement-focused savings advantage

This makes APY useful not only for pension planning but also for tax-saving purposes.

Experts suggest that salaried individuals with modest income can combine APY with other investment instruments like Public Provident Fund (PPF) and National Pension System (NPS) for better retirement planning.

What Happens After the Subscriber’s Death?

Atal Pension Yojana also provides financial security for families.

If the subscriber dies after retirement:

- The spouse continues receiving the pension

- After the spouse’s death, the accumulated pension corpus goes to the nominee

If the subscriber dies before age 60:

- The spouse can continue the scheme

- Or exit the scheme and claim accumulated funds

This family protection feature makes APY especially valuable for households dependent on a single earning member.

Digital Banking Has Boosted APY Enrollment

The rapid expansion of digital banking infrastructure in India has significantly helped APY grow.

Today, citizens can enroll through:

- Public sector banks

- Private banks

- Post offices

- Net banking platforms

- Mobile banking apps

The auto-debit contribution system ensures that monthly payments are deducted directly from the subscriber’s bank account, reducing the risk of missed contributions.

Government campaigns promoting financial inclusion and digital banking have further improved awareness about pension schemes among rural populations.

APY vs Other Retirement Schemes

Many people compare APY with other retirement and investment schemes available in India.

Here is how APY differs:

APY vs National Pension System (NPS)

- APY offers guaranteed pension

- NPS returns depend on market performance

- APY is simpler for small contributors

- NPS provides potentially higher long-term returns

APY vs Public Provident Fund (PPF)

- PPF focuses on savings and returns

- APY guarantees monthly pension income

- PPF has flexible withdrawal options

- APY emphasizes retirement security

APY vs Employees’ Provident Fund (EPF)

- EPF is employer-linked

- APY is open to self-employed and informal workers

- APY targets unorganized sector employees

Financial planners often recommend APY for individuals without formal retirement benefits.

Women and Rural Workers Driving Growth

Recent enrollment trends indicate strong participation from women and rural workers.

Experts believe several factors contribute to this trend:

- Growing financial awareness among women

- Self-help groups promoting pension enrollment

- Rural banking expansion

- Government outreach programs

- Increased focus on social security

Many women working in self-employment or informal occupations are now opting for APY to ensure independent retirement income.

This represents an important shift toward long-term financial planning in rural India.

Challenges Still Exist

Despite strong growth, APY still faces some challenges.

Key issues include:

- Low awareness in remote areas

- Irregular income among informal workers

- Contribution defaults due to financial instability

- Limited pension amount compared to inflation

Some financial experts argue that the ₹5,000 maximum pension may become insufficient in the future due to rising living costs.

There have also been discussions about increasing pension limits and improving flexibility for subscribers.

Why Retirement Planning Matters More Than Ever

India’s growing workforce and changing economic conditions have increased the importance of retirement planning.

Traditionally, many families depended on children for post-retirement support. However, urbanization, migration, and rising living expenses are changing family structures rapidly.

As a result:

- Personal retirement savings are becoming essential

- Pension coverage gaps remain large

- Informal workers require social security protection

Schemes like Atal Pension Yojana are therefore becoming increasingly important for long-term financial stability.

How to Apply for Atal Pension Yojana

The enrollment process is simple and accessible.

Applicants need:

- Aadhaar card

- Mobile number

- Savings bank account

- Basic KYC documents

They can visit:

- Banks

- Post offices

- Online banking portals

The subscriber chooses:

- Pension amount

- Contribution frequency

- Nominee details

After activation, contributions are automatically deducted from the linked bank account.

APY Subscriber Numbers Continue Rising

According to recent government data, APY subscriber numbers continue growing steadily every year. Millions of Indians have already enrolled, making it one of the country’s largest pension inclusion programs. (pfrda.org.in)

The government expects further expansion as awareness campaigns continue across rural and semi-urban regions.

Financial experts believe APY could play a major role in reducing old-age financial insecurity in India over the coming decades.

Final Verdict

Atal Pension Yojana has become one of India’s most important social security initiatives for the unorganized sector. By offering guaranteed pension benefits, low contribution requirements, and government-backed reliability, the scheme provides millions of Indians with a practical path toward financial security after retirement.

As economic uncertainty and inflation continue affecting households, retirement planning is no longer optional. For low and middle-income earners seeking a stable and affordable pension solution, APY remains one of the strongest government-backed options available today.

With rising enrollment numbers and growing awareness, Atal Pension Yojana is steadily transforming how millions of Indians prepare for life after retirement.